SA's Fibre Underdogs Are Beating the Giants

Ispa's February 2026 survey of 45 ISPs found six smaller fibre network operators outscoring six of the country's eight biggest names. Here's what the ratings actually measure, why Vumatel jumped and Link Africa slid, and what it means for your next fibre signup.

In this article(10)

- 01A report card most fibre customers never see

- 02What Ispa actually measured, and why ISPs are the right people to ask

- 03The 2026 scoreboard: Octotel on top, Vumatel still last among the majors

- 04The real headline: six smaller networks are quietly outscoring the giants

- 05Why smaller networks are winning on service, even if they can't win on reach

- 06Vumatel's biggest jump of the year - and why it's still last

- 07The Maziv group is done integrating and is expanding again

- 08Meanwhile, township fibre is rewriting who counts as a major network at all

- 09What this actually means for your next fibre signup

- 10Frequently asked questions

A report card most fibre customers never see

Every fibre line in South Africa has two companies behind it: the internet service provider (ISP) that bills you and answers your support tickets, and the fibre network operator (FNO) that owns the physical cable running past your house. You choose the ISP. You almost never choose the FNO - it's determined by whichever network happened to trench fibre down your street. Webafrica, Afrihost, MWeb and dozens of smaller ISPs all resell the same handful of underlying networks: Openserve, Vumatel, MetroFibre, Octotel, Frogfoot, Link Africa, Liquid Intelligent Technologies and Dark Fibre Africa, plus a longer tail of smaller regional players.

Because consumers rarely interact with the FNO directly, there has never been an easy way to know which networks are actually good to be on. That's the gap the Internet Service Providers' Association of South Africa (Ispa) has spent the last three years trying to close, by asking the one group of people who deal with FNOs constantly and have no reason to flatter them: the ISPs themselves.

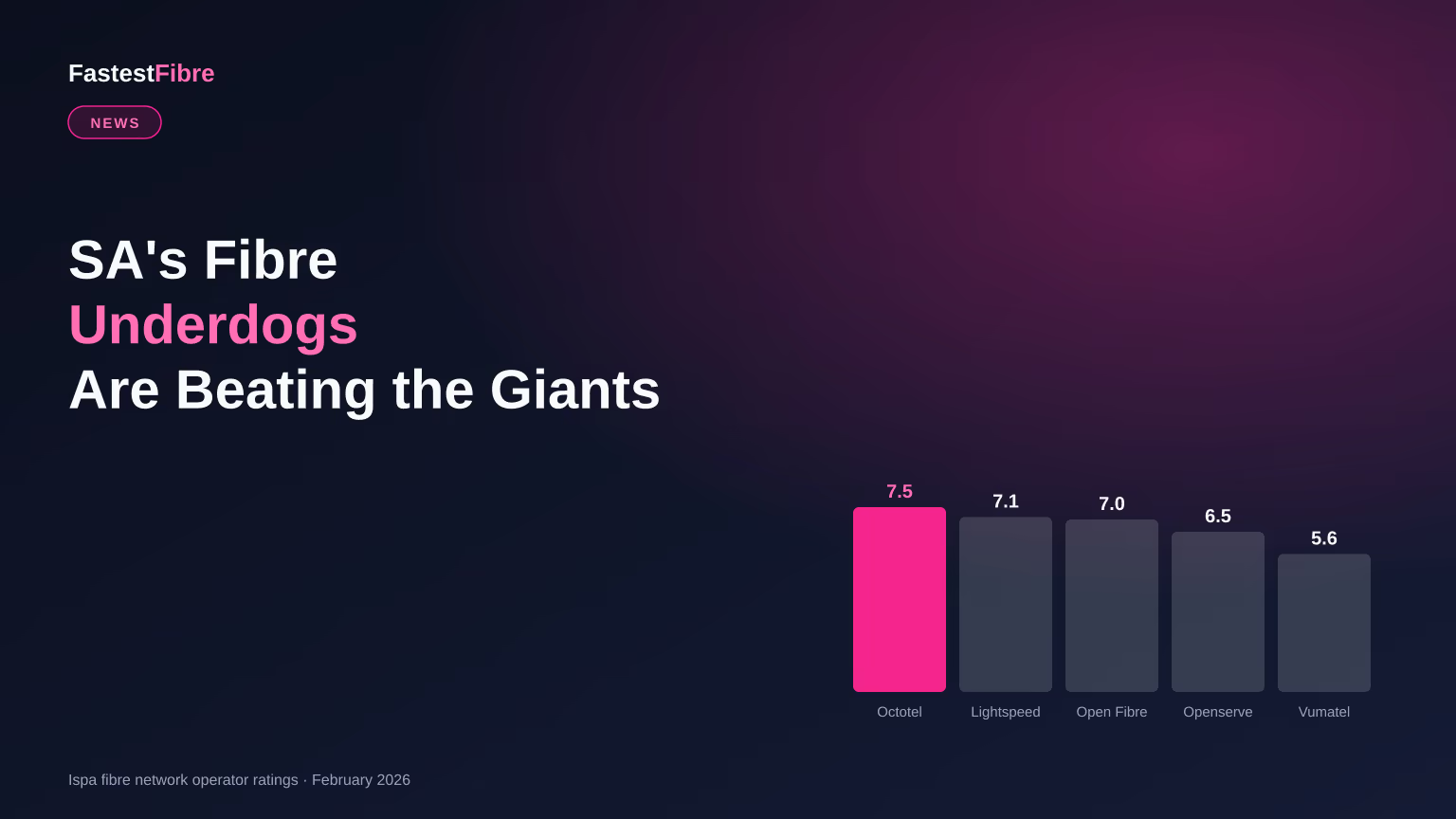

The association's latest rating round, run in February 2026, produced its most interesting result yet. Six smaller network operators that most consumers have never heard of - Lightspeed (the network arm of ISP Cybersmart), Open Fibre, Lightstruck, Evotel, Seacom FibreCo and WeCom - all scored higher than Vumatel, the country's biggest fibre network by homes passed, and higher than five of the other seven major operators too. Only Octotel, the survey's overall leader, beat all six of them.

Ispa's own framing was blunt. "When smaller firms start outperforming their bigger industry compatriots, that's something to watch and it bodes well for future service levels," Ispa spokesperson Ant Brooks said of the results. This piece walks through exactly what the survey measured, where each major network landed, why the underdogs are winning, and - because a satisfaction score means nothing if you can't act on it - what it should change about how you shop for fibre in 2026.

What Ispa actually measured, and why ISPs are the right people to ask

Ispa has been running this perception survey since 2023, asking its member ISPs to score every FNO they deal with across 11 separate criteria, each on a 0-10 scale: reliability, technical proficiency, staff friendliness, open-access adherence (whether the network genuinely treats every reseller equally), value for money, communications, support, business processes, software systems, likelihood of recommendation and optimism about future improvement. Each FNO's headline score is the average across all 11.

The February 2026 wave gathered 406 individual ratings from 45 participating ISPs - up from 355 ratings the previous year, which Ispa reads as more ISPs engaging with more networks as the market keeps fragmenting. That fragmentation is itself a legacy of Vumatel's open-access model, which from the start let any ISP resell its fibre rather than forcing a single retail arm - a structure that's since spread across the industry and is a large part of why South Africa has more than 75 active fibre ISPs rather than a handful of vertically-integrated telcos.

Why trust ISPs to grade FNOs fairly? Because they're a genuinely adversarial audience. An ISP's margin, support-ticket volume and churn rate are all downstream of how well its upstream network performs, so it has every commercial incentive to rate networks honestly rather than diplomatically. Ispa itself flags the one real limitation of the method: for the smaller, less-rated networks, "less likely to reflect the opinions of all" users, since a score built from eight or ten ISPs carries more noise than one built from thirty-eight. That caveat matters for reading the underdog results below, and we'll come back to it.

Nationally, ISPs said the four metrics they weigh most heavily - unchanged from the year before - were reliability, staff friendliness, technical proficiency and open-access adherence. In other words: does the network stay up, are the humans on the other end of the phone competent and pleasant, and does the network treat this ISP the same way it treats every other reseller on the same infrastructure. Notably absent from that top-four list: raw price. ISPs are telling Ispa that a network being difficult to work with costs them more than a network being slightly more expensive.

The 2026 scoreboard: Octotel on top, Vumatel still last among the majors

Among the eight most-rated networks - the ones with enough ISP responses that Ispa is confident in the number - the February 2026 results were:

- Octotel - 7.5/10 (+0.1 year-on-year, rated by 18 ISPs)

- Openserve - 6.5/10 (-0.2, rated by 38 ISPs - the widest reach of any network)

- MetroFibre - 6.4/10 (-0.3, rated by 31 ISPs)

- Liquid Intelligent Technologies - 6.1/10 (unchanged)

- Frogfoot - 6.1/10 (+0.5, its best result in three years)

- Link Africa - 5.8/10 (-0.3, its lowest score since the survey began in 2023)

- Dark Fibre Africa - 5.8/10 (+0.9, also its best result in three years)

- Vumatel - 5.6/10 (+1.0 - the single biggest year-on-year gain of any network rated)

The average score across all rated networks came in at 6.2/10, essentially flat on the year. But the averages hide two very different stories moving in opposite directions. Vumatel's score improved by a full point - the largest single-year jump anyone recorded - yet it still finished last among the eight majors, because it was climbing out of an unusually weak prior-year base. Link Africa moved the other way: a modest 0.3-point drop looks minor until you notice it's now the network's worst score since Ispa started measuring in 2023, a sign the decline has been gradual rather than a one-off dip.

Zoom out two years and the churn becomes even clearer. In the February 2024 wave, Openserve topped the table outright at 7.0, MetroFibre and Link Africa both sat above 6.8, and Vumatel and Frogfoot were mid- pack in the 5-6 range. Two years on, Octotel - a modest riser in 2024 - has taken over the top spot, Openserve has fallen a full half-point from its 2024 peak, Link Africa has slid from a co-leader position to second-last, and Frogfoot has climbed from the bottom half into a tie for fourth. None of the eight majors' relative rankings from 2024 survived intact into 2026.

What's driving those swings isn't public in granular detail, but Ispa's category breakdowns from the 2024 round give a hint of the pattern: technical proficiency, value-for-money, reliability and support consistently separate winners from laggards, and account-manager quality "significantly influenced" how ISPs scored an individual network overall. A network's engineering can be sound while a handful of under-resourced account teams still drag its score down - which is exactly the kind of soft-skills problem that's easier for a smaller, leaner operator to avoid than a network servicing three or four times as many resellers.

The real headline: six smaller networks are quietly outscoring the giants

Below the eight most-rated majors, Ispa also published scores for six smaller operators that don't yet have enough ISP relationships to sit in the primary leaderboard, but which crossed the minimum threshold to be included this year:

- Lightspeed (Cybersmart) - 7.1/10, rated by 11 ISPs

- Open Fibre - 7.0/10, rated by 12 ISPs

- Lightstruck - 7.0/10, rated by 10 ISPs

- Evotel - 6.9/10, rated by 8 ISPs

- Seacom FibreCo - 6.9/10, rated by 8 ISPs

- WeCom - 6.6/10, rated by 11 ISPs

Line those six up against the major-network scoreboard and the result is striking: every single one of them would place in the top two positions of the eight-network leaderboard, ahead of Openserve, MetroFibre, Liquid, Frogfoot, Link Africa, Dark Fibre Africa and Vumatel - all seven, in every case except Octotel itself. Evotel's 6.9 isn't a new phenomenon either; it was already the standout smaller network back in the February 2024 round at 7.5, alongside Zoom Fibre's network arm at 7.4, so this isn't a single lucky survey wave - smaller operators have out-punched their size for at least two consecutive rating cycles.

Ispa's own read on this is that it's a genuine market signal, not statistical noise: "when smaller firms start outperforming their bigger industry compatriots, that's something to watch and it bodes well for future service levels," Brooks said, adding that the trend of more, smaller networks earning solid ratings "suggests that ISPs are steadily using more fibre operators to deliver more services and the implications for free competition are clear."

That said, the caveat from the methodology section deserves repeating here rather than glossing over: these six scores are each built from eight to twelve ISP responses, versus 18 to 38 for the major networks. A smaller sample doesn't make a score wrong, but it does make it more sensitive to a single unusually happy or unhappy ISP relationship, and it means none of these six networks has yet been tested at the scale Openserve or Vumatel operate at - tens of thousands of active ports and support tickets a month, across every province, rather than a handful of metro pockets. A network that impresses 10 ISPs servicing a few suburbs hasn't necessarily proven it can hold that standard once it's serving 40 ISPs and a million homes. Whether these underdogs can keep their scores up as they scale into that territory is the actual open question - and it's one only the next two or three survey cycles will answer.

Why smaller networks are winning on service, even if they can't win on reach

There's a structural reason smaller FNOs tend to outscore giants on exactly the metrics ISPs say matter most - reliability, staff friendliness, technical proficiency and open-access adherence - and it has little to do with better engineering and a lot to do with headcount ratios. A network with 10 ISP partners can staff a handful of account managers who genuinely know every reseller's account history, escalation contacts and network topology by name. A network with 38 ISP partners, serving well over a million connected homes, is running a call-centre-scale support operation instead - and Ispa's own findings point squarely at account-manager quality as a major swing factor in how an ISP scores its upstream network.

Scale also multiplies the surface area for things to go wrong. A network with a few thousand active lines in one or two metro pockets has a small, homogenous footprint to keep healthy. A network with homes passed in the millions, stretching from premium Sandton streets to rural feeder routes and densifying township deployments, is managing wildly different infrastructure ages, splice quality and fault-repair logistics under one brand - and every one of those variables shows up somewhere in an ISP's reliability or technical-proficiency score.

None of this means bigger networks are bad networks. Openserve, the wholesale arm of Telkom, still pulls the widest ISP participation of any network measured (38 raters) precisely because it's the network most ISPs actually resell somewhere in the country - reach that none of the six underdogs above currently match. Being rated by more ISPs, across more edge cases and more geographies, is itself a harder test to pass consistently. It's the difference between a boutique restaurant with a five-star rating from forty regulars and a national chain holding four stars across four hundred locations - the chain's job is objectively more difficult to do consistently well.

Vumatel's biggest jump of the year - and why it's still last

Vumatel's trajectory deserves its own explanation, because "last among the majors" and "most improved network of the year" are both true at once, and the context connects directly to the biggest structural story in South African fibre right now: consolidation. Vodacom completed a R11 billion deal for a 30% equity stake in Maziv - the holding company that now sits over Vumatel, Vodacom Fibre, Dark Fibre Africa and, as of a Competition Tribunal approval in December 2025, Herotel too - on 1 December 2025.

Folding four previously separate organisations under one group inevitably creates a period of internal friction: merging support systems, aligning account-management processes across newly combined ISP relationships, and integrating network operations teams that were built to run independently. A dip in ISP-facing service quality during exactly that kind of integration year, followed by a sharp recovery once the dust settles, is a very ordinary pattern for a company absorbing acquisitions this large - and it lines up with Vumatel logging its lowest-ever score in the survey wave before this one, then posting the largest single-year improvement of any network in the wave that followed.

Dark Fibre Africa's own +0.9 jump to a three-year high tells a similar story from the infrastructure side: the company replaced 12,000km of ageing metro fibre with newer technology in the period covered, on top of 12,600 already-connected sites, while its fibre-to-business connections grew 9% to just under 55,000. Physical network investment of that scale takes time to show up in day-to-day reliability - but it's exactly the kind of spending that eventually moves a satisfaction score, and it appears to be starting to.

The Maziv group is done integrating and is expanding again

The clearest sign that Maziv's post-merger integration phase is winding down is its own language about what comes next. "We have to start expanding again, start building the way we used to build," CIVH (Maziv's parent) chief executive Dietlof Mare said of the group's plans, framing the next phase around South Africa's "untapped, unconnected market" rather than further consolidation.

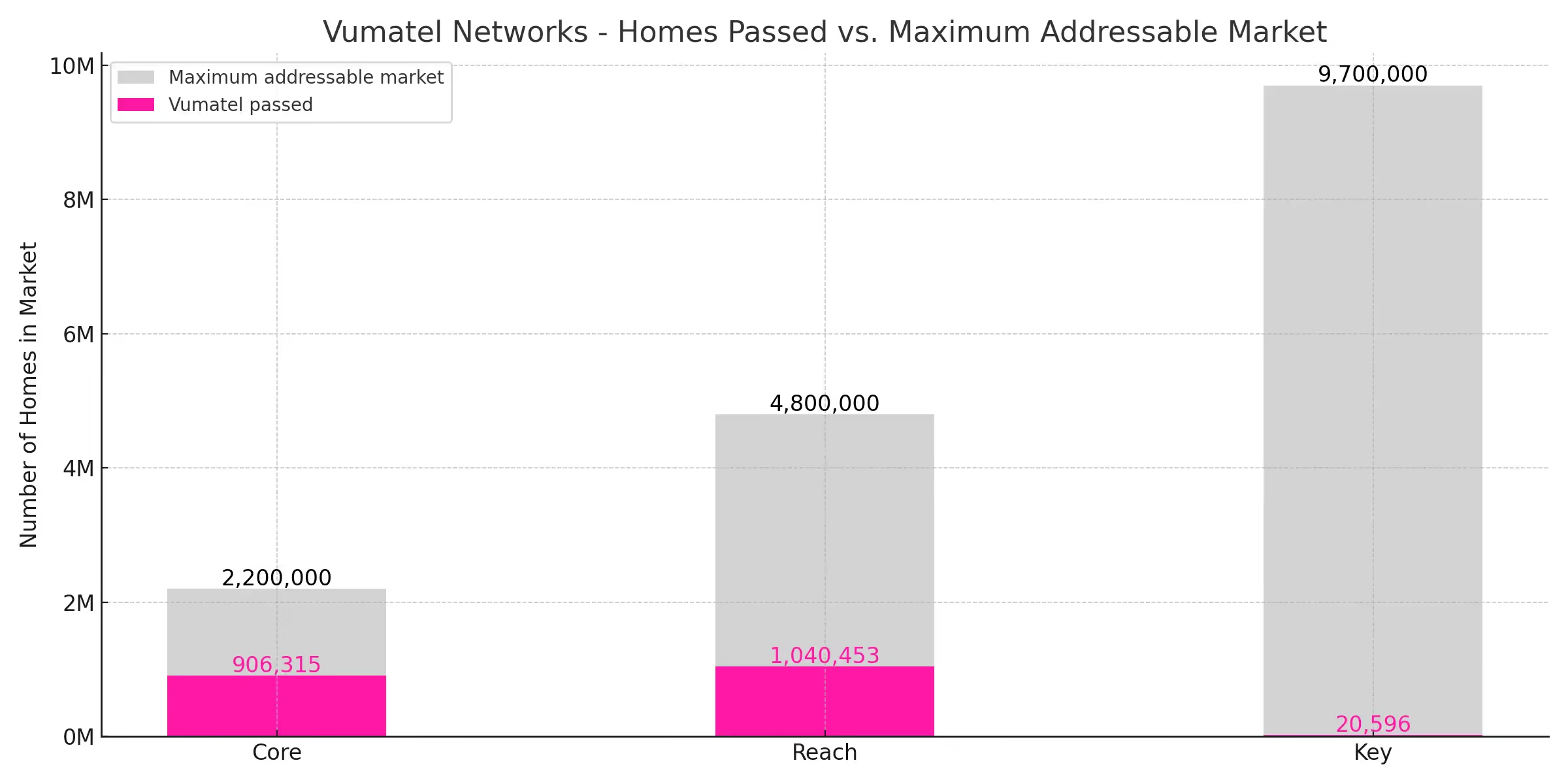

The numbers back that framing up. Vumatel passed 200,000 new homes in its most recent reporting period and has committed to the Competition Commission - as a merger condition - to build one million additional homes, with an explicit focus on the "Reach" and "Key" product tiers built for lower-income households rather than the premium suburbs the network built its early reputation on. Financially, CIVH's revenue grew 11% to R3.76 billion, Vumatel's own revenue rose 15% to R2.17 billion, and free cash flow before capital expenditure - the money actually available to fund that next million homes - climbed 31% to R1.5 billion.

For consumers, the practical read is straightforward: the network most likely to newly reach your street over the next year or two isn't a scrappy independent - it's Vumatel, backed by Vodacom's balance sheet and explicitly instructed by competition regulators to grow into underserved areas as a condition of the deal that created Maziv in the first place. Whether that expansion arrives with the improved service levels the February 2026 score suggests, or reverts under the strain of another growth phase, is worth watching in next year's Ispa results.

Meanwhile, township fibre is rewriting who counts as a major network at all

While the Ispa survey measures wholesale relationships between FNOs and ISPs, a parallel and arguably more consequential shift has been happening at the retail end of the market: prepaid, pay-as-you-go fibre built specifically for township and lower-income households, where a traditional 24-month contract and credit check were never a realistic product.

Fibertime, founded by Alan Knott-Craig, sells uncapped fibre through R5-a-day vouchers bought at spaza shops - no contract, no credit check, no monthly debit order. The network now has 470,000 connected homes across 53 townships in 13 cities and seven provinces, up from roughly 10,000 homes in March 2024 - growth of well over 40x in about two years. That scale already makes Fibertime, in Knott-Craig's words, "by far the biggest township FNO" in the country and the third-largest fibre network operator overall by connected homes, behind only Vumatel and Openserve. Fibertime advertises 100Mbps uncapped as standard, but has already demonstrated 1Gbps downloads with 560Mbps uploads and 14ms latency on its upgraded Alexandra network, and plans to upgrade every network it operates nationwide over the next 12 months.

Herotel has taken a related but distinct path, becoming South Africa's largest retail FTTH ISP by connected homes - a different measure to the wholesale FNO ratings above, since Herotel is customer- facing rather than a pure network operator, and (following the Competition Tribunal's approval of Vumatel's acquisition in December 2025) now sits inside the same Maziv group as Vumatel itself. Herotel counts 284,850 connected FTTH customers plus 52,094 fixed-wireless customers, for more than 350,000 total active customers across 550-plus towns, with 612,000 homes already passed and ready to connect. Like Fibertime, Herotel deliberately targets smaller towns, peri-urban areas and township communities rather than established metro suburbs - areas where, according to the company, customers are consuming over 1TB of data a month at roughly R0.50 per gigabyte on a prepaid, top-up-like-airtime model. "Whether people can afford to stay connected and use that connection for school, work, business, communication and entertainment without constantly managing data limits" is how chief executive Van Zyl Botha framed the company's affordability focus - and Herotel is targeting 1.1 million homes and roughly six million people, with 750,000 of the additional homes specifically in townships.

None of the six wholesale underdogs in Ispa's survey operate primarily in this prepaid, township segment - but the pattern rhymes. In both cases, the operators winning right now are the ones that picked a specific, underserved slice of the market and built a lean operation tightly matched to it, rather than trying to be all things to all ISPs and all households at once.

What this actually means for your next fibre signup

It's worth being precise about what an Ispa score can and can't tell you. It cannot tell you which network is available at your address - that's still purely a function of which FNO happened to trench fibre down your specific street, and no satisfaction survey changes that. What it can tell you is something ISPs themselves rarely volunteer in marketing material: which networks are pleasant to be a reseller on, which correlates reasonably well with how quickly faults get fixed, how accurate coverage and installation information tends to be, and how much friction you'll hit if something goes wrong.

Three practical takeaways follow from the 2026 results. First, if you have a genuine choice of network at your address - increasingly common as Vumatel, Openserve, Frogfoot and others overlap in more metro areas - Octotel's leading score is a real, independently-sourced data point worth weighing alongside price and speed, not just a marketing claim. Second, don't write off Vumatel because of last year's lower scores; a full-point year-on-year recovery, on top of an explicit regulator-driven commitment to expand into underserved areas, suggests the post-Maziv integration friction is easing rather than compounding. Third, if a smaller network like Evotel, Lightstruck, Open Fibre, Seacom FibreCo, WeCom or Lightspeed happens to be the operator behind an ISP deal you're considering, treat a 6.6-7.1 score as a genuinely good sign, with the honest caveat that a network scored by ten ISPs hasn't yet been tested at the scale a giant like Openserve has.

Beyond the network layer, the ISP you choose still matters just as much - the same underlying fibre line can feel completely different depending on how quickly your ISP answers a support ticket, whether it ships a usable router, and what its contract terms actually allow. Check what's available at your address, compare live pricing across the ISPs that resell whichever network reaches you, and use survey data like this as one more input rather than the only one.

Frequently asked questions

Help someone else pick the right fibre

Related insights

Icasa's 2026 ICT Report: Fibre Grew 22%, SA Fell 13 Places Globally

Read article

Vuma Key vs Fibertime: SA's Prepaid Fibre Showdown

Read article

The Maziv Merger Explained

Read article

Openserve vs Vumatel in 2026

Read article

Vumatel Hits One Million Subscribers

Read article