Vumatel Hits One Million Subscribers: What This Milestone Actually Means for South African Fibre

Vumatel crossed the one million connected subscriber mark in February 2026, eight years after launch. Here's what the milestone says about the South African fibre market.

In this article(7)

A milestone reached faster than ADSL ever managed

In February 2026, Vumatel announced that it had crossed one million connected fibre-to-the-home subscribers. The headline got the usual industry coverage - press release, MyBroadband write-up, LinkedIn celebration - and then quickly settled into the news cycle. But the milestone deserves more attention than it received, because of what it tells us about the speed of broadband adoption in South Africa, the shape of the fibre market, and where growth is now coming from.

Vumatel founded its FTTH operation in 2014 and launched its first connections shortly afterwards. Reaching one million connected customers in roughly eight years places it well ahead of the previous fixed-line technology benchmark in South Africa. ADSL, the copper-based broadband technology that Telkom rolled out in the early 2000s, took approximately 14 years to reach its peak of just over one million subscribers. Vumatel hit the same number in just over half the time, on a more demanding technology that required physical fibre cable to be trenched into every connected home.

The market matured faster than analysts predicted

When fibre rollouts began in earnest in South African suburbs around 2015, the prevailing analyst view was that FTTH would saturate the top LSM bands quickly and then struggle to grow. The thinking was that South African households outside the wealthier suburbs would either skip fibre in favour of mobile data, or take longer than expected to adopt. That view proved to be partially correct and partially wrong.

It was correct that early fibre growth came overwhelmingly from premium metro areas - Sandton, Bryanston, Constantia, Rondebosch, Durban North, Umhlanga. By 2020, those areas were largely saturated. The view was wrong about what came next. Rather than stagnating, Vumatel's growth shifted to a different segment of the market entirely: townships, secondary suburbs, and historically underserved communities. This shift was driven by the Vuma Reach product, which lowered the price of fibre entry to the point where it became a viable alternative to mobile data for households where data costs are a significant share of monthly spend.

According to Maziv CEO Dietlof Maré, much of Vumatel's recent subscriber growth has come from these traditionally underserved areas. That's a meaningful structural change in the market. It means fibre is no longer just a premium service for high-income households - it's becoming a mass-market utility.

The competitive picture in 2026

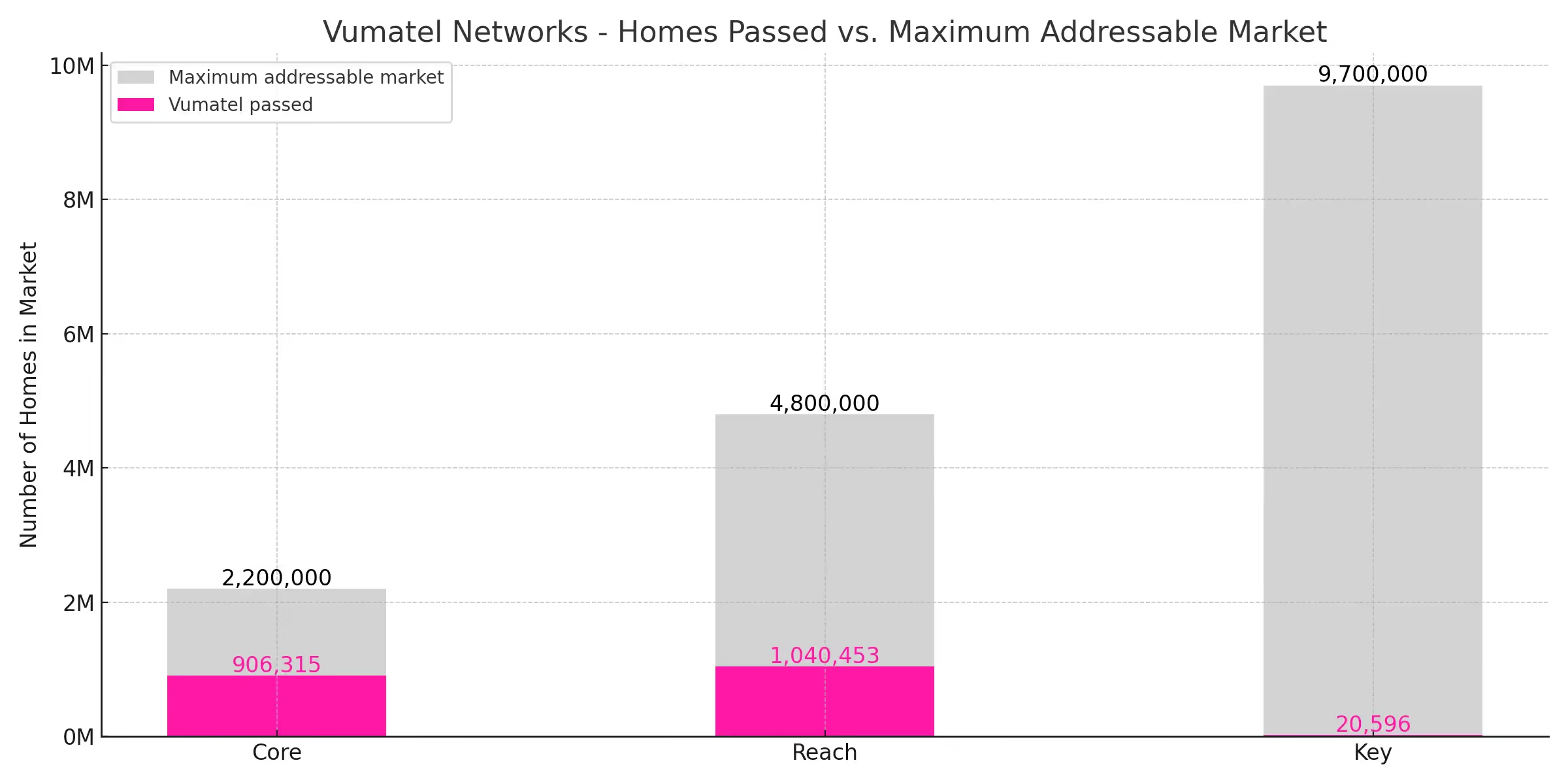

Vumatel is now the largest FTTH provider in South Africa by both homes passed and homes connected. It accounts for approximately 36 percent of the FTTH market, almost double the share of the next closest competitor.

Its main competitor is Openserve, the Telkom subsidiary that operates the legacy copper and modern fibre network. As of March 2025, Openserve had passed approximately 1.38 million homes and connected around 694,000 customers. Openserve has a higher fibre connectivity rate (the percentage of passed homes that actually take a fibre service) at over 50 percent, but a smaller absolute customer base. Openserve is also more dependent on fibre revenue as a share of group operating revenue, which influences how aggressively it can compete on price.

Other operators - Octotel, Frogfoot, MetroFibre, MTN Fibre, Lightstruck, Evotel, Zoom, Clearaccess - operate in specific geographic footprints or focus on particular building/estate categories. None individually approaches Vumatel's scale.

Growth driven by Reach

The single most important factor in Vumatel's growth between 2023 and 2026 has been the Vuma Reach product. Reach was designed specifically to extend fibre into communities where the standard FTTH economics don't work - where average household spend on connectivity is too low to support traditional FTTH pricing, where banking penetration is lower (so debit order billing fails), and where contract-based products have historically struggled.

Reach addressed those constraints with three product decisions. First, prepaid payment via EasyPay vouchers, eliminating the need for a debit order. Second, an integrated ONT/router (lower hardware cost). Third, a simpler speed range, which reduced both marketing complexity and ISP onboarding cost.

The product worked. Reach has become the engine of Vumatel's recent subscriber growth, and it's the model the rest of the market has been trying to copy. Vodacom's prepaid fibre plans (effectively a partner rebrand of Reach via Vumatel infrastructure) launched in 2025 with packages starting at R249/month, explicitly framed as an anti-digital-divide initiative.

What one million customers tells us about price elasticity

There's a useful economic insight in the way Vumatel's subscriber base grew. The first half-million customers came largely from price-tolerant, high-income households who wanted speed and reliability and weren't deeply price-sensitive. The second half-million came from a much more price-sensitive market segment, where a R150 price difference per month materially changes household decisions.

That suggests the South African fibre market still has significant headroom - but only for products priced appropriately for the next segment of households. The next million subscribers will not come from premium suburbs. They will come from secondary and tertiary towns, township areas, and rural service centres, served by products priced at or below R400/month.

The challenge ahead

Vumatel's next phase isn't about repeating what worked. The premium suburb playbook is finished - there are very few streets in Sandton, Constantia, or Rondebosch where Vumatel hasn't already passed every house. The Reach playbook still has runway, but it operates on much thinner margins per subscriber and requires continued capex to extend network into new areas.

The economics of that next phase depend heavily on:

- How quickly the merged Maziv group can extract operational efficiencies from the combined Vumatel/Vodacom Fibre/DFA/Herotel footprint

- Whether Icasa's merger conditions allow flexibility in product pricing and segmentation

- Whether mobile data prices fall further, eating into the affordable-fibre opportunity

- Whether load shedding remains stable enough that fibre's value proposition holds up against mobile alternatives

What it means for households

If you're a fibre customer in 2026, the practical implications of Vumatel reaching one million customers are mostly positive. Scale brings ISP choice (more than 75 ISPs now resell Vumatel), better support infrastructure, faster fault response times, and continued network investment. It also brings competitive pressure on price - every ISP on the network is fighting for a slice of an increasingly crowded retail market, which keeps headline prices honest.

The risk side is concentration. With one operator at 36 percent of the market and consolidating further through Herotel, regulatory oversight matters more than it did when the market was fragmented. Icasa's conditions on the Maziv merger are designed to address exactly that risk, but their effectiveness will only become clear over the next two to three years.

For now, the milestone is what it looks like: a sign that fibre has moved from premium niche to mass-market infrastructure in South Africa, and that the next decade of growth will look very different from the last one.

Help someone else pick the right fibre

Related insights

The April 2026 Openserve Price Increase: What Changed and What It Means for Your Bill

Read article

Did Webafrica Buy MWeb? What It Means for Your Fibre

Read article

MWeb vs Afrihost 2026: Which SA Fibre ISP Is Better?

Read article

Is MWeb Fibre Worth It in 2026? An Honest Review

Read article